Social Security Strategy: Claim Early or Wait? The Numbers Don’t Lie

Deciding when to claim Social Security can significantly shape retirement income. Learn how important factors can affect your strategy.

Deciding when to claim Social Security can significantly shape retirement income. Learn how important factors can affect your strategy.

Use a mid-year business checkup to review revenue, cash flow, staffing, and personal wealth before year-end decisions become more difficult.

DIY investing may seem simple, but hidden costs can add up. Learn how investor behavior, taxes, time and planning gaps can affect long-term returns.

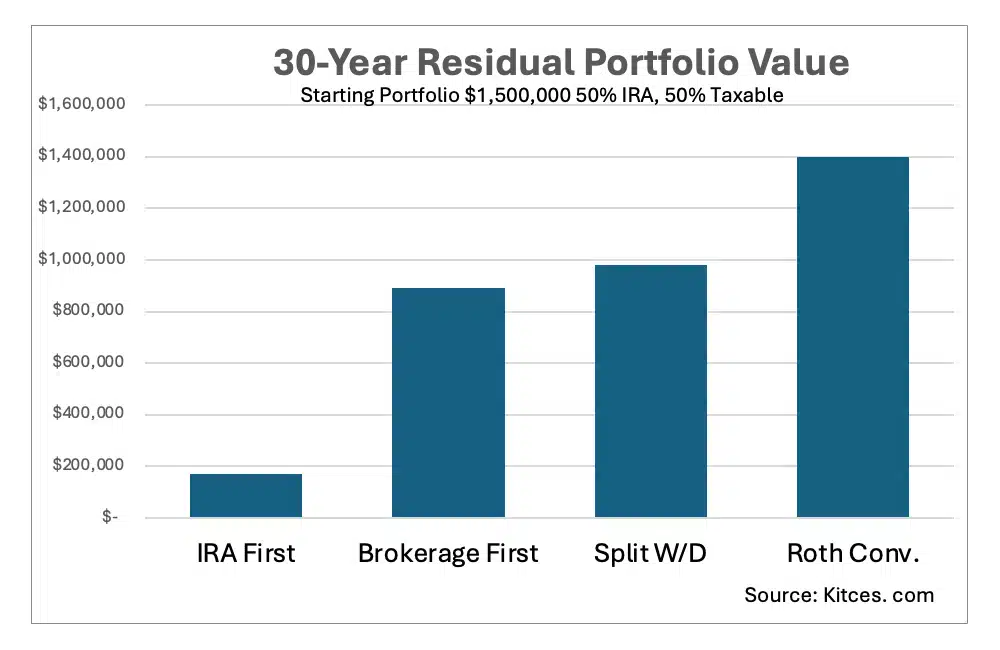

Learn when a Roth IRA or Roth conversion may make sense, and how taxes, Medicare premiums, charitable goals, and estate planning can affect the decision.