The Importance of Training (and Planning)

Carelessness and overconfidence can derail both flying and finances. Discover why training and planning are essential for long-term success.

Carelessness and overconfidence can derail both flying and finances. Discover why training and planning are essential for long-term success.

Market volatility and headlines can drive emotion. Discover why disciplined investors stay focused on long-term results.

Not all retirement accounts are the same. Explore IRA vs. 401K differences and how they impact your taxes and income.

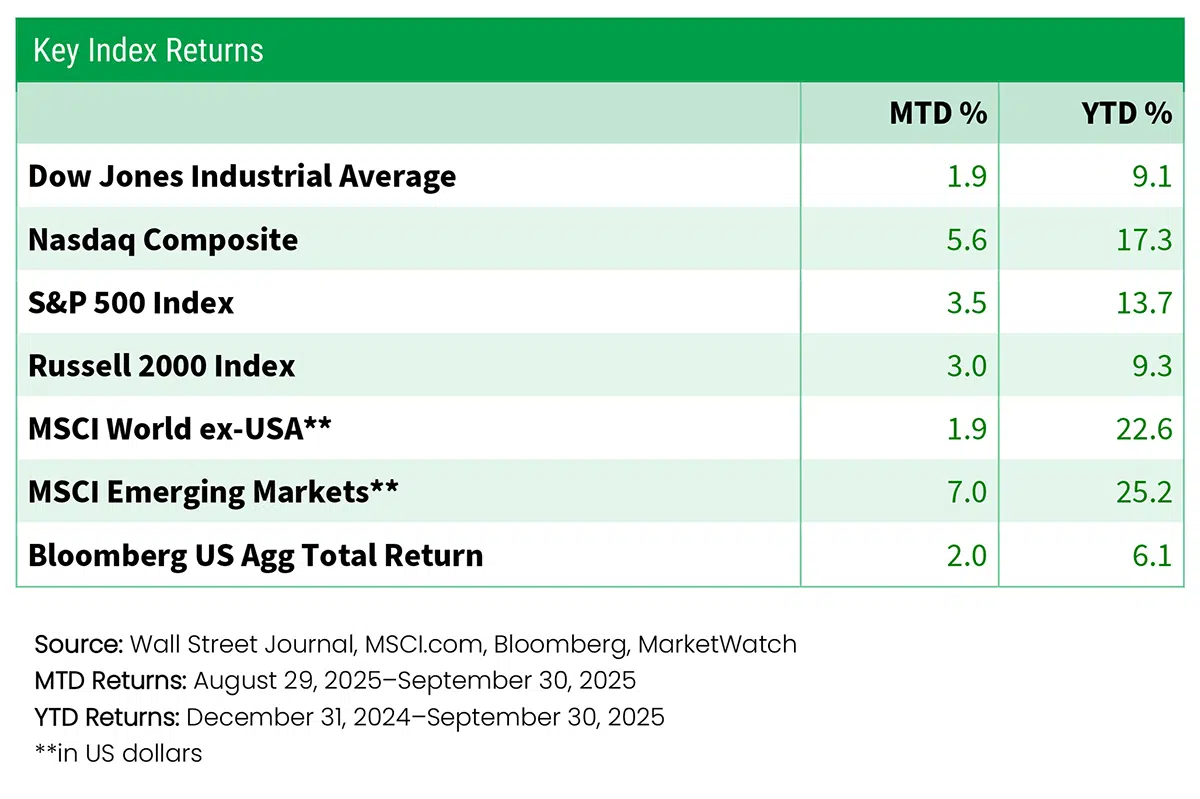

What does the Dow reaching 50,000 mean for investors? Explore market breadth, earnings trends, and valuation signals shaping today’s markets.