1) IRS Audit

What certifications or credentials does a cost segregation “professional” need?

Believe it or not, the answer is NOTHING! Given that it’s your signature on the tax return and thus your liability, it is crucial you research any firm you may use for your study. The American Society of Cost Segregation Professionals offers a directory of Certified professionals with exam and experience requirements. Choosing the right firm helps to improve the odds of ensuring that the benefit exceeds the cost (cost of payment to the vendor AND cost of liability).

Red Flag Alert – You cannot DEPRECIATE LAND – recently we analyzed a cost segregation study where the firm severely underestimated the value of the land so they could promote excess tax savings. Don’t be deceived by this type of inflated marketing!

The government knows what your incentive is; this strategy needs to be implemented properly. Shortcuts now could make those tax savings vanish with penalties and fees later.

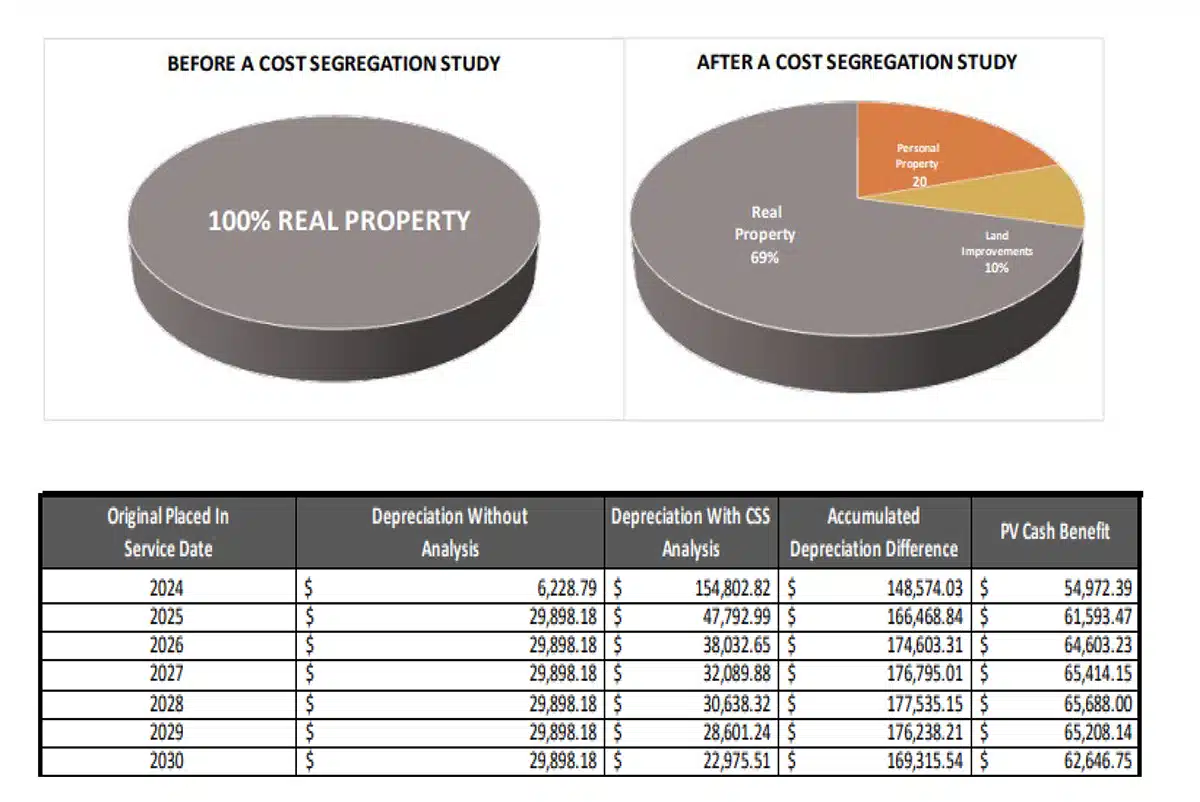

2) IMPACT on your overall wealth accumulation plan.

A crucial distinction to highlight is the amount of total depreciation does not change whether you use straight line or accelerate your depreciation schedule. This strategy shines as a timing mechanism to shift your depreciation to be advantageous to you. It is a time value of money puzzle that can be optimized for your benefit.

3) Understanding your tax rate now and in the future.

Do you know what your tax rate is? …. Probably not. We do! We review every client’s tax return. If you do not know what your tax rate is, it’s not feasible to determine if this strategy is worthwhile.

I’ll refer to this as the depreciation trap. Let’s say you are in the 22% or 24% marginal tax bracket, is front loading depreciation going to benefit you? Maybe, but not as likely as those in the 32%, 35% and 37% brackets.

Your unrecaptured gain is taxed as ordinary income up to 25%. This provision surprises many taxpayers.

So as an example, if you are in the 37% bracket and do a cost segregation, you are shielding income taxed at 37% and if you sold the property in the next year your unrecaptured gain would be capped at 25%. It is tax arbitrage with a 12% differential. Let’s say you accelerated $300,000 this year and then you sold the property the next year. Your spread would be $36,000 depending on your tax rates the following year.

What if you are in a lower tax bracket with lots of allowable depreciation and then you sell in a year when gains are plentiful does the government care? No, they don’t, your unrecaptured gain is based on the year of disposition. Wait, so I could shield income at 12% and 22% and pay up to 25% on the sale? Indeed, and that is the depreciation trap.

4) Understanding depreciation recapture provisions.

We cannot delve into the mechanics in this newsletter, but a cursory understanding of recapture is vital. When you take a depreciation deduction against your ordinary income, eventually this will become an unrecaptured gain in the future. Your basis is reduced by the allowable depreciation. It is known as a recharacterization of gain when you sell the real property. This gain is not taxed at favorable capital gains tax rates. This gain is taxed as ordinary income up to 25%. Section 1245 and 1250 are complex and every scenario has nuance especially with a cost segregation as you are changing the character of 1250 property to accelerate your depreciation.

The Solution(s):

Find the right broad-based and experienced thinking partner/personal CFO to help you navigate decisions that are IMPACTful to you and your family.

Your Success Team advisors need to collaborate when you implement this strategy. The focus should be on the long game; not just the current tax year. Don’t let the tax tail wag the dog.

You could have substantial savings from using cost segregation, but it takes an evidence-based approach as well as a well-aligned Success Team to make sure it’s done right for you.